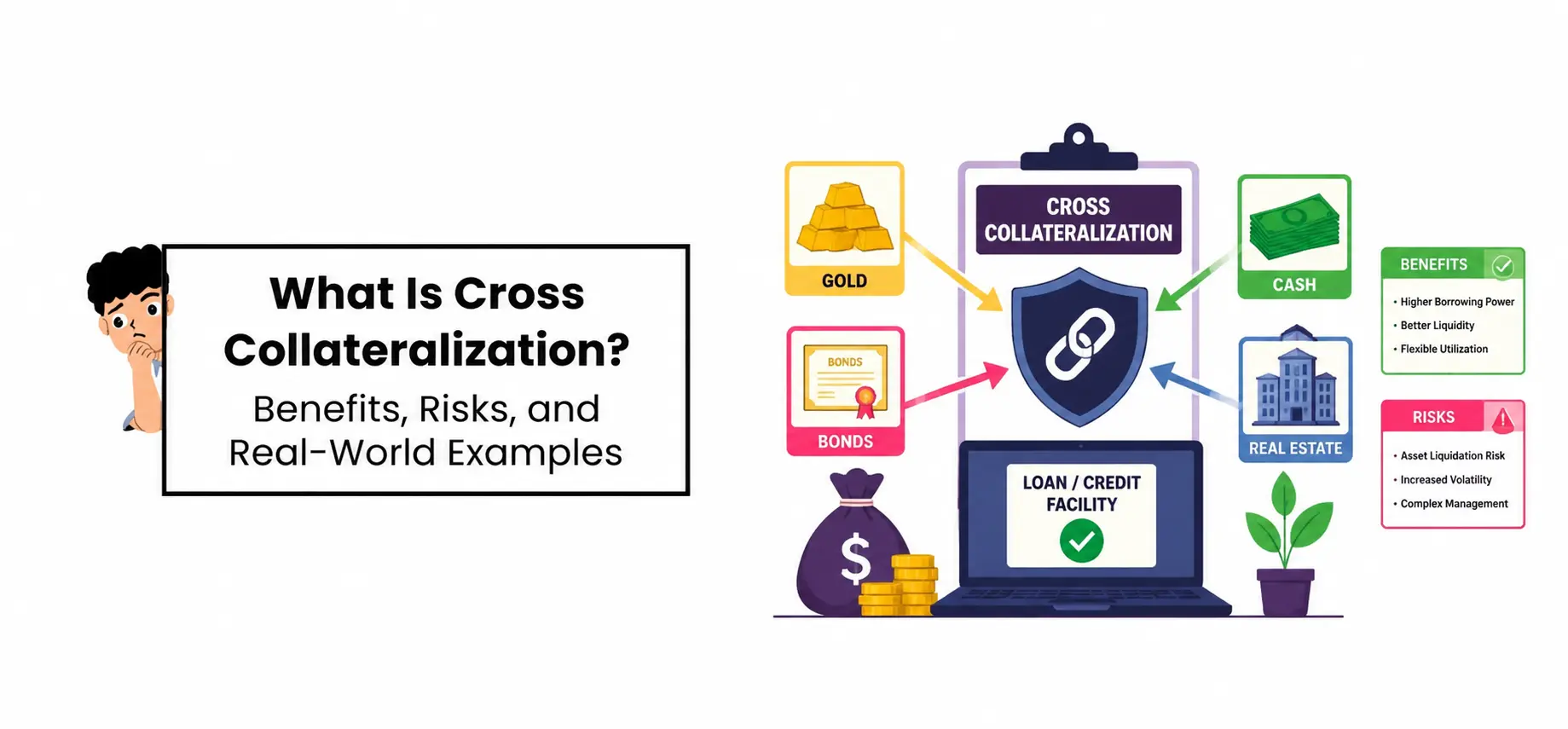

What Is Cross Collateralization? Benefits, Risks, and Real-World Examples

When applying for a loan , lenders often ask borrowers to provide an asset as security. In a way, it kinda helps lower the lender’s risk, if the borrower cannot repay the money. Sometimes, a lender might allow the same property to secure more than one loan , so, that relationship gets called cross collateralization.

Cross collateralization can help borrowers access additional funds, yet it also brings risks that shouldn’t be brushed off. If you understand how it operates, it becomes easier to decide what borrowing approach makes sense for individuals or a business.

In this guide, we will walk through cross collateralization in simpler terms, cover its pros and cons, and go over a couple of real-world situations, so you can judge if this arrangement fits your own financial picture.

What Is Cross Collateralization?

Cross collateralization is a lending arrangement where one asset is used to secure multiple loans from the same lender. Instead of giving a different property to each loan, the lender sort of leans on the same property, vehicle, equipment, or investment account as security for more than one debt obligation, you know in the background.

For lenders, this can reduce risk since they end up with a stronger claim on the borrower’s assets. For borrowers, it can make funding feel more attainable, because there may not be a need to line up extra assets.

For example, a homeowner could use the equity in their home to obtain a mortgage, then later use the same home as backing for another loan. If either loan turns bad or just goes unpaid, the lender may have the right to seize the property.

Understanding the Role of Collateral in Lending

Before digging deeper into cross collateralization, it helps to understand what collateral means, plain and simple.

A collateral loan is a kind of borrowing where the borrower pledges an asset to ensure repayment. If the borrower defaults, the lender can take ownership of that asset to recover losses.

Some typical forms of collateral include :

- Homes and real estate

- Vehicles

- Savings accounts

- Stocks and investments

- Business equipment

- Inventory

Collateral helps lenders feel steadier when approving loans, because the debt is supported by a valuable asset.

Secured vs. Unsecured Borrowing

Not all loans need collateral. In general, lending tends to sort itself into two groups: secured and unsecured.

A secured loan asks for an asset as security. Since the lender has that extra coverage against losses, these loans often end up with lower interest rates and usually higher borrowing ceilings, too.

Unsecured loans , like a lot of personal loans and credit cards, don’t ask for collateral. Because the lender is taking on more risk the rates are often higher.

Borrowers who have valuable assets may see secured borrowing as an appealing option, not just because it might help the approval process, but also because it can trim the overall borrowing costs.

How Cross Collateralization Works

Cross collateralization kind of works like a simple chain of events.

First, the borrower pledges an asset to get financing. Later, the lender might let that same asset stand behind more borrowing. Instead of making separate security documents for each new debt, the lender basically ties several obligations to one asset.

That asset then stays attached to all of the promises until the debts are paid in full.

This setup becomes especially significant when you talk about loan collateral, because one single piece of property or other asset may end up covering multiple financial commitments at the same time.

So, borrowers should really know, with care, how their property is being used before they sign any financing agreement.

Multiple Loans Secured by One Asset

A pretty common example of cross collateralization is when multiple loans share one collateral setup, like it is a single umbrella, but they are not really the same deal.

Just imagine a small business owner, they have company equipment and they use it to back a business expansion loan.

A year later, that same lender comes back and offers another line of credit, again with that equipment sitting there as security, even if the wording feels a bit different.

So, basically both loans are tied to the very same asset. If the borrower can not keep up with payments on either one of the debts, the lender can end up with rights over the equipment. And that is the whole point, it leads to higher financial exposure than if each obligation was secured with separate collateral, because then one problem would not automatically spill into the other one.

That is why borrowers should, before signing, really think through how much of their overall debt is connected to a single asset. It sounds small at first, but the overlap can become a real issue later.

Benefits of Cross Collateralization

Cross collateralization can come with a handful of benefits when it’s used, honestly, in a responsible manner. Sometimes it feels like there are more doors open than it looks like at first.

Easier access to funding

Borrowers may end up qualifying for larger loans, lenders usually like the extra security they’re getting. For companies trying to push growth, this added backing can be a big deal, not just a small “maybe” thing.

Lower interest rates

Because the lender’s risk is reduced, borrowers may get more favorable rates and terms compared to borrowing without that backing, unsecured style.

Faster loan approval

If collateral already exists, approval can move along quicker. Borrowers might not need to chase or document brand new assets for each financing request.

Support for business expansion

A lot of the time, businesses use cross collateralization as a sort of asset-backed loan approach. Equipment, inventory, or commercial property might help unlock more capital for growth plans.

More financial flexibility

When it’s managed properly, borrowers can sometimes access funding opportunities that otherwise would be pretty much off limits.

Still though, these positives should always be balanced against the potential downsides, even if it seems all smooth at the start.

Risks and Disadvantages of Cross Collateralization

But cross collateralization isn’t all sunshine , it can also bring serious financial trouble.

Greater asset exposure

The main concern is that one asset ends up backing several debts. If repayment turns messy , the borrower could end up losing an important asset that was tied to multiple obligations at once.

Limited freedom

Trying to sell or refinance a cross-collateralized asset can become difficult, since the lender still has an interest in the property. So it’s not as “your call” as people assume.

More complex debt management

These setups often involve several obligations, and that means the borrower has to monitor things carefully, not just sign and forget.

These risks become especially important in secured lending situations where borrowers might lean heavily on pledged assets to obtain financing. Without solid planning, borrowers may get overextended, and then the whole arrangement starts to feel like it’s closing in.

Understanding Loan Security Risks

The idea of loan security is kinda central to cross-collateralization, lenders see it as a main point. In general, collateral is treated as protection against default. That part does help lenders lower their losses, but borrowers end up taking on extra risk since their own assets can get exposed if financial troubles pop up.

Like, say a borrower suddenly loses income unexpectedly and then misses payments. In that case the lender might move to legal action involving the collateral. So yeah, borrowers should really look at worst-case scenarios first, before they sign any financing arrangement, even if it sounds straightforward. A loan that looks manageable today, can turn into a problem later if the situation changes.

Understanding Cross Default Clauses

Also, a lot of cross-collateralized loans include a cross default clause. Basically, this lets a lender treat one missed payment as a default across several loans at once. For example, if someone misses payments on a business loan, the lender might declare a default on a different revolving line of credit that’s also backed by the same collateral. Because of that, borrowers can get serious consequences even when only one obligation becomes shaky. Reading every contract term, and not just the shiny parts, is essential before accepting financing.

Why Loan Agreement Terms Matter

Borrowers should watch the loan agreement terms very closely whenever collateral is part of it, no skipping.

Some key questions to ask include:

- Which assets are being pledged?

- How many loans are tied together through that collateral?

- Can collateral be released once repayment happens.

- What events count as a default?

- What lender rights actually apply?

Getting clear on those points can help avoid expensive surprises later on. It may also be wise to use professional legal or financial support when reviewing complicated loan agreements, because details can get kinda slippery.

Real-World Examples of Cross Collateralization

Example 1: Home Equity Borrowing

A homeowner uses their house, to secure a mortgage. Later they get a home equity loan, from the same lender, and it’s tied to that same property too. So the home ends up holding both obligations, sort of at the same time.

Example 2: Business Expansion

A company leans on machinery, to get financing for expansion. Then later the lender okays extra borrowing, but it’s backed again by the same equipment. This kind of collateral based arrangement can help momentum, yet it also adds exposure when income falls, even a little.

Example 3: Real Estate Investment

An investor has a handful of rental properties and uses them to back multiple loans. Cross collateralization can open the door to larger capital, but it also might trip things up if the property values slide.

Example 4: Vehicle Financing

Some lenders may group a vehicle loan with other credit products under one collateral arrangement. In that situation, borrowers should read the contracts closely, to figure out how these pieces connect.

When Cross Collateralization May Make Sense

Cross collateralization may make sense when:

- Income stays steady.

- Overall debt is under control.

- The extra funds go toward useful, productive investments.

- Borrowers really understand the downside, not just the upside.

Businesses often use this approach to reach growth capital without buying extra assets. Still, thoughtful planning matters a lot.

When Borrowers Should Avoid It

Cross collateralization is a financing strategy that allows one asset to secure multiple loans. It can help borrowers access larger amounts of funding, receive better interest rates, and simplify the borrowing process. However, it also increases risk because a single asset may be tied to several debts.

Before entering a cross-collateralized arrangement, borrowers should understand the collateral involved, review all loan terms carefully, and consider the potential consequences of default. With proper planning and responsible borrowing, cross collateralization can be a useful financial tool, but it should always be approached with caution.

Best Practices Before Signing

Before agreeing to a cross collateralized loan, go through every paper pretty carefully, and make sure you understand every repayment obligation too.

- Try to work out the potential risks in real terms.

- Then compare what different lenders are offering, don’t just stick with the first option.

- If you feel unsure, ask for professional financial advice.

- Also confirm what happens to the collateral once repayment is done, not just what the marketing says.

These kinds of steps can help borrowers choose more intentionally and reduce avoidable financial strain

Conclusion

Cross collateralization is basically a financing approach where one asset can stand as security for more than one loan. This may allow borrowers to get bigger funding, sometimes obtain steadier interest terms, and overall make borrowing seem simpler. But at the same time, it raises the stakes, because the same asset could end up connected to several debts.

If you are thinking about a cross collateralized setup, you really should grasp which collateral is involved, review every loan condition closely, and think through what could happen if there is a default. With smart planning and sensible borrowing, cross collateralization can be a helpful financial instrument, yet it should still be handled with caution, and not treated like a casual decision

Understand lending and finance with confidence. Visit Market Investopedia for expert insights, practical guides, and market knowledge to support smarter financial decisions.

FAQ

Cross-collateralisation is basically lending arrangement, where one asset is used to back multiple loans a the same time. If the borrower ends up defaulting on any one of those loans, then the lender can go after the collateral thats shared, sort of claim it.

For example, a homeowner might put their house up as collateral for a mortgage, then later they also take out a home equity loan using the same property. So the home is backing both arrangements, even if they were signed at different times.

In the banking world, cross-collateralization means a lender is using one asset to secure several obligations. This usually makes the lender a bit more protected, but it can also make the borrower’s risk higher, because the asset could be on the line across multiple debts, not just one.

You should look through your loan agreement for phrases like “cross-collateralization” or “cross-default” and don’t just skim past it. Then ask your lender something direct like, whether the collateral tied to one loan also covers other commitments or future obligations.

In finance terms, cross collateralization is the approach where a single asset acts as the surety, for several loans or credit lines. It can help borrowers obtain more financing because the lender has more reassurance.

How it works: one asset is linked to several loans, and the collateral stays pledged until all the related debts are paid off, in line with what the lender requires.

Cross collateralization can improve approval odds, expand borrowing capacity, make the setup simpler, and in some cases, it might even help interest rates, since lenders get that extra security.

Category :

Share :